Class of 2013 Debt and Income Survey Results

Posted By Heather , Apr 9, 2013

Last week, the King Hall Student Budget Committee created a survey for current 3Ls to anonymously report their debt and expected income. You can see the full survey below. This post will report our findings from that survey and provide some commentary.

Ninety eight 3Ls responded to our survey, this is 49% of the class. While I was aiming for a higher response rate, the number of responses is still significant enough to report our findings and useful in understanding the current status of the Class of 2013.

DEBT

Quartiles and Average Current Debt for the Class of 2013

- Minimum: 0

- 25%: $63,843.25

- Median: $108,500

- 75%: $140,000

- Maximum: $208,000

- Average: $98,588.56

INCOME

DEBT TO INCOME

Collecting data about debt and income gives a broad brush picture of the value the Class of 2013 received from King Hall. However, in deciding if law school is a good investment or not, the real inquiry should be in debt to income, or how much of your monthly income will be consumed by debt payments. To my knowledge, there has been no survey of law students focusing on this question. We have income surveys, and debt surveys, but no one has asked the same question in one survey to be able to compare each person's debt to income in a graduating class and analyze the ability of the class to pay back their loans, until now.

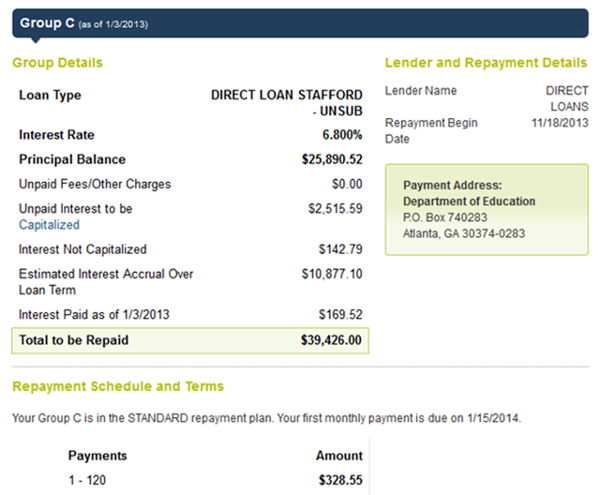

First, some methodology. Here is the full excel spreadsheet containing the survey responses and my calculations. I started with the reported debt in the far left hand column. I went on my loan service provider's webpage (nelnet.com) to look at the calculation of my monthly payments for each of my loans. Here is an example of how one of my loan's monthly payments was calculated:

I took the total monthly payment for each loan and added it together to get my total amount due to service my debt every month. I divided my total debt by my total monthly payments for all my loans. This gave me the number of 1.1956%. In other words, about 1% of my total loans will be due each month, starting in December 2013, for the next ten years (the standard repayment plan).

I took each reported total debt and multiplied by 1.1956% to find each person's total monthly payment to service that debt. This assumes that most people will have a combination of loans with interest rates similar to mine. The range of interest rates for federal loans is 6.8%-7%. Therefore, I do not think my calculation of monthly payments based is based on too big of an assumption because the interest rate difference between the available loans is not significant.

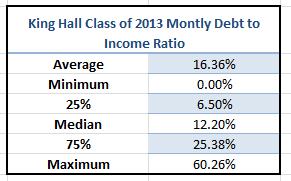

I averaged the reported expected income range and divided by twelve to find expected monthly income. I then divided each monthly debt payments by the corresponding reported monthly income. This results in the percentage of each respondent's monthly income that will be used to service his or her debt. Here are the distributions for the Class of 2013 Monthly Debt to Income Ratio for those who responded to the survey and reported an income:

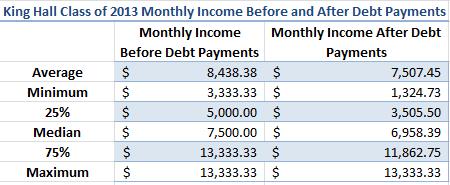

At the town hall, it was suggested that I subtract the monthly debt payments from the corresponding monthly incomes to picture how monthly income will be depleted by monthly debt payments. Here are those calculations:

As was predicted at the town hall, the change from $13,333 to $11,862 a month does not feel as significant from $5,000 to $3,505 monthly salary. So the significance of the debt to income ratio may depend on your expected salary.

There are two points to keep in mind when looking at these calculations. First, it was a small sample size. Of the 98 survey respondents, only 38 reported any salary. As I can't divide a monthly debt payment by zero, I could only calculate the debt to income ratios for those 38 who reported a salary.

Second, these ratios are probably low compared to the actual class debt to income ratios. If the Class of 2013 follows about the same employment pattern of the Class of 2012,

full statistics listed here, my reported salaries are high.

We had 11 people report a salary of $150,000-169,000 (or 28% of the reported salaries). The Class of 2012 had a total of 17 people report a salary of $160,000 nine months after graduation (or 8% of the reported salaries). If the Class of 2013 employment nine months after graduation shifts to look more like the Class of 2012, as anecdotal evidence suggests, our survey accounted for most of the higher earning students in our class and class income profile is currently skewed high. Students who will report income nine months after graduation are not likely to be in the $160,000 range, but in a lower bracket.

This is due to legal market hiring cycles. All law schools' reported employment rate is lower at graduation than nine months after graduation. Some employers wait until after bar results are released in November to make employment offers. However, the employers who tend to do this are not those at the top end of the salary range. Therefore, those who report having a job before graduation are likely to report a higher salary then those who obtain jobs in the summer or after the bar.

Factoring in those who will obtain employment after the bar would likely increase the average debt to income of the class because those with a lower income would likely have a higher debt to income ratio. This would not be true if those who are not reporting income now have below average debt. Based on our survey responses shown in the excel sheet, there does not seem to be a correlation between low debt and no job, so this is not likely to be the case. Instead, it is likely that the numbers reported above are likely skewed low, and the actual debt to income of the class is slightly higher nine months after graduation.

There is much more to be said about our survey results. To stop this post from becoming unwieldy long, I'll cut it here with one last point. Anyone who is seriously considering or analyzing law schools should do so carefully. There are many articles either damning law schools or upholding them as pillars of higher education. The reality is much more complex. A place to start should be profiling each graduating class's debt to income at graduation, nine months after graduation, and every year after that.

Having an accurate picture of the debt to income ratio of each class is the only way to seriously analyze if a law school is a good investment; if the students are able to manage their debt after graduation.To my knowledge, I have never seen a survey or publication look at the debt to income ratio of law students. If anyone knows of one, I'd love to see it. This should not be an effort of one student group at one law school. The collection and publication of this data should be demanded by all who have a stake in law school.